Every Budget season brings the same confusion: “Is my income completely tax-free now?” The 2025 Union Budget’s headline zero tax on income up to ₹12 lakh set off a wave of half-right interpretations. Some taxpayers assumed they owed nothing. Others were hit with unexpected bills.

Here is the complete, accurate picture of Section 87A of the Income Tax Act for FY 2025-26 (AY 2026-27), covering both regimes, with the latest CBDT clarifications included.

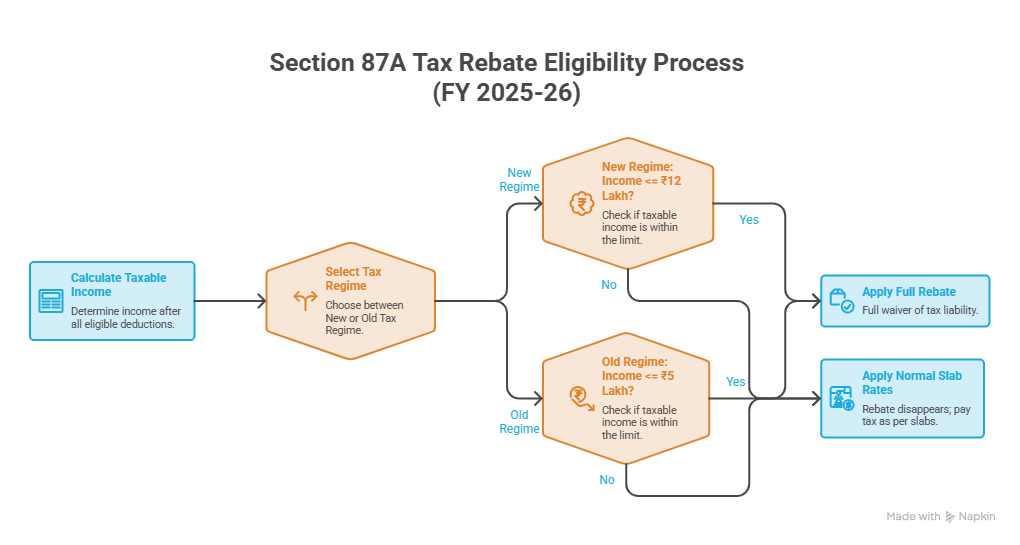

Section 87A provides a direct rebate against your calculated income tax, but only if your taxable income stays within a specified limit.

It is not a tax rate cut for everyone. It is a full waiver of tax liability for those below the threshold. The moment your taxable income crosses that threshold by even ₹1, the rebate disappears entirely and normal slab rates apply in full.

For FY 2025-26, the rebate limits are:

| Tax Regime | Max Rebate | Rebate If Taxable Income Is Up To |

|---|---|---|

| New Tax Regime default | ₹60,000 | ₹12,00,000 |

| Old Tax Regime | ₹12,500 | ₹5,00,000 |

Remember: The rebate applies on taxable income, that is, your income after all eligible deductions. Gross salary and taxable income are not the same number.

The Budget 2025 expanded the Section 87A rebate under the New Tax Regime from ₹25,000 FY 2024-25 to ₹60,000, making taxable income up to ₹12 lakh completely tax-free. The new regime is now the default regime for all individual taxpayers.

| Taxable Income Slab | Tax Rate |

|---|---|

| Up to ₹4,00,000 | Nil |

| ₹4,00,001 to ₹8,00,000 | 5% |

| ₹8,00,001 to ₹12,00,000 | 10% |

| ₹12,00,001 to ₹16,00,000 | 15% |

| ₹16,00,001 to ₹20,00,000 | 20% |

| ₹20,00,001 to ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

These slab rates apply uniformly to all individuals regardless of age under the new regime.

Salaried employees and pensioners under the new regime are entitled to a standard deduction of ₹75,000. This means if your gross salary is ₹12,75,000, your taxable income after the standard deduction is exactly ₹12,00,000 and the rebate fully applies. For salaried individuals, the practical zero-tax threshold is ₹12.75 lakh.

Under Section 87A, your tax liability jumps sharply the moment taxable income crosses ₹12 lakh. This is the “cliff effect.”

Without marginal relief: A taxable income of ₹12,10,000 would attract slab tax of ₹61,500, with no rebate, meaning ₹10,000 of extra income costs ₹61,500 in tax.

With marginal relief available under the new regime: The additional tax payable is capped at the amount by which your income exceeds ₹12 lakh. So for ₹12,10,000 of taxable income, the tax payable is restricted to ₹10,000, not ₹61,500.

Marginal relief is automatic and built into the new regime. It does not apply under the old regime. This is one of several reasons why choosing between the two regimes is a decision that benefits from careful modelling, especially if you have deductions to weigh. Read our detailed guide on

tax-efficient wealth management strategies for HNIs

to understand how regime selection fits into your broader tax picture.

If you opt for the Old Tax Regime, the Section 87A rebate remains unchanged at ₹12,500, with a taxable income threshold of ₹5 lakh. The standard deduction under this regime is ₹50,000 for salaried employees.

| Taxable Income Slab | Tax Rate |

|---|---|

| Up to ₹2,50,000 | Nil |

| ₹2,50,001 to ₹5,00,000 | 5% |

| ₹5,00,001 to ₹10,00,000 | 20% |

| Above ₹10,00,000 | 30% |

Senior citizens 60 to 79 years: Basic exemption limit is ₹3 lakh. Super senior citizens 80+ years: ₹5 lakh.

This is the most commonly misunderstood aspect of Section 87A in FY 2025-26.

The Finance Act 2025 and a subsequent CBDT clarification February 2026 explicitly state:

The Section 87A rebate, including the enhanced ₹60,000 rebate under the new regime, is not available against tax computed on income taxed at special rates, specifically:

Practical impact: If your total income is ₹10 lakh, comprising ₹8 lakh salary and ₹2 lakh STCG from equity, the rebate applies only to the slab tax on ₹8 lakh. The ₹2 lakh STCG is taxed separately at 20%, and that tax cannot be offset by the 87A rebate.

Taxpayers with equity investments, mutual fund redemptions, or property sales must calculate their tax liability carefully and not assume the “zero-tax up to ₹12 lakh” headline applies to their full income. If your portfolio generates regular capital gains, understanding

can help you structure investments in a way that reduces unplanned tax exposure.

The new regime offers fewer deductions, but these still apply:

If you are a salaried professional navigating these choices, our

can help you model the optimal regime based on your exact income and deduction profile.

If your taxable income is slightly above ₹5 lakh, these deductions can help bring it within the rebate limit:

For a comprehensive breakdown of how these deductions interact with your retirement savings strategy, read our guide on

tax planning for retirement in India

.

Retirement-focused investors should also note that these deductions, particularly 80C and NPS, are directly tied to long-term wealth building. Our guide on

covers how to integrate tax efficiency with your overall corpus-building plan.

The Section 87A rebate is genuinely powerful but it comes with conditions that most headlines skip. Know your taxable income, not just your gross salary. Know which regime you are in. And if you have equity investments, understand that your capital gains are taxed separately.

Given the tax cliffs at both the ₹5 lakh and ₹12 lakh marks, small income oversights can cost tens of thousands of rupees. Start your tax planning early in the financial year, not in the final weeks of March. High-income earners and HNIs with multiple income streams will particularly benefit from proactive planning. Explore how

at Right Horizons addresses tax strategy as part of a holistic financial plan.

Want a personalised tax plan?

Connect with a Right Horizons financial advisor

to model both regimes for your income, deductions, and investment profile.

Talk to us

Investor Grievance

Talk to us

Investor Grievance