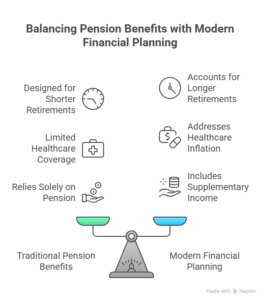

Government employees in India have access to a set of retirement benefits that most private-sector workers simply do not: pension, gratuity, GPF, and leave encashment. But these benefits, while valuable, were designed for a time when life expectancy was lower, and retirement lasted at most a decade.

Today, with retirements stretching over 25-30 years and medical costs inflating by 8-14% annually, relying solely on your pension is not enough. Comprehensive financial planning for government employees must go beyond entitlements. It must account for inflation, longevity risk, healthcare costs, and supplementary income. The pension scheme for government employees has itself evolved, with the Unified Pension Scheme now fully operational from April 2025, and new benefits such as the Fixed Medical Allowance being aligned across schemes as recently as March 2026.

Understanding what you are entitled to and how to build on it is the foundation of a secure retirement.

For central government employees who joined service before 1 January 2004:

For employees who joined on or after 1 January 2004:

The Unified Pension Scheme, introduced by the Government of India and operational from 1 April 2025, is the most significant pension reform for central government employees in two decades. It sits within the NPS architecture and is regulated by PFRDA.

What changed in 2026: In March 2026, the DoPPW issued an Office Memorandum dated 13.03.2026 extending Fixed Medical Allowance benefits to all UPS-covered employees, putting them on equal footing with NPS employees. New investment options, Life Cycle 75 and Balanced Life Cycle, have also been extended to both NPS and UPS subscribers.

As per PFRDA and the Ministry of Finance:

Eligibility: Existing NPS employees as of 1 April 2025, new recruits, and retired NPS subscribers with a minimum of 10 years of service. The option deadline was 30 November 2025. Once opted, UPS is irrevocable. Check with PFRDA or your department for any extended timelines.

Gratuity is a one-time lump sum, one of the most significant retirement benefits for government employees in India.

The General Provident Fund is a mandatory, government-backed savings scheme for employees who joined before 1 January 2004.

| Feature | Detail |

|---|---|

| GPF Interest Rate: Q4 FY 2025-26, Jan-Mar 2026 | 7.1% p.a. – Ministry of Finance Resolution, 9 Jan 2026 |

| GPF Interest Rate: Q1 FY 2026-27, Apr-Jun 2026 | 7.1% p.a. – Ministry of Finance, April 2026 |

| Minimum Contribution | 6% of the basic salary per month |

| Maximum Contribution | 100% of salary, up to ₹5 lakh per year |

| Tax Benefit | Contributions up to ₹1.5 lakh under Section 80C; interest and maturity fully tax-free |

| Withdrawal | After 15 years of service or within 10 years before retirement |

| Loan Facility | Available at 2.5% above the GPF interest rate |

The General Provident Fund interest rate has remained at 7.1% p.a. since FY 2020-21. The Ministry of Finance, Department of Economic Affairs, Budget Division, confirmed this for both Q4 FY 2025-26 and Q1 FY 2026-27.

Leave encashment is the payment received for unused earned leave upon retirement. It is one of the lesser-understood yet high-value retirement benefits for government employees.

Leave encashment rules for central government employees:

Leave encashment calculation formula: Leave encashment amount = Basic Pay + DA at retirement ÷ 30 × Number of accumulated leave days

Note: For private-sector employees, leave encashment tax exemption is capped at ₹25 lakh under Section 10(10AA). Government employees have no such cap; the entire amount is exempt.

Pension commutation allows retiring government employees to convert up to 40% of their monthly pension into an upfront lump sum:

Tax planning is an integral part of financial planning for government employees, and one of the most effective levers to protect retirement wealth. Here is a consolidated view of how government employees can legally minimize their tax burden, both during service and at retirement:

| Retirement Benefit | Tax Treatment |

|---|---|

| Monthly Pension | Taxable as Income from Salary |

| Commuted Pension, Lump Sum | Fully exempt – Section 10(10A) |

| Retirement Gratuity | Fully exempt – Section 10(10) |

| Leave Encashment Tax Exemption | Fully exempt – Section 10(10AA) |

| GPF Maturity | Fully exempt |

| NPS Lump Sum Withdrawal, 60% | Exempt – Section 10(12A) |

| NPS / UPS Annuity | Taxable as income |

As per CBDT OM dated 02.07.2025:

Understanding these provisions is among the most impactful income tax saving strategies for government employees, particularly because gratuity, leave encashment, and GPF maturity together can amount to several lakhs at retirement, all of which may be fully tax-free if structured correctly.

| Factor | NPS | Unified Pension Scheme |

|---|---|---|

| Pension certainty | Market-linked; not guaranteed | Assured at 50% of the average last 12 months’ basic |

| Inflation protection | Depends on corpus growth | Dearness Relief indexed to AICPI-IW |

| Minimum pension | Not guaranteed | ₹10,000/month, 10+ years of service |

| Lump sum on exit | 60% of the corpus, tax-free | 1/10th of emoluments per 6 months + gratuity |

| Family pension | Annuity plan dependent | 60% of pension |

| Fixed Medical Allowance | Eligible | Eligible, confirmed March 2026 |

| Best suited for | Higher risk tolerance, longer service | Those prioritising pension predictability |

As of 2026, with the Fixed Medical Allowance now extended to the Unified Pension Scheme, the case for UPS is stronger for employees seeking an assured, inflation-indexed income. Employees with long service and higher salaries should consult a certified financial planner before making this irrevocable decision.

Even with a pension, gratuity, GPF corpus, and leave encashment, finding the best investment plan for government employees means building supplementary income sources that are low-risk, tax-efficient, and inflation-aware. Here are the most suitable options, government-backed and otherwise:

Yes, central government employees can invest in mutual funds, subject to conduct rules. Under the CCS Conduct Rules, 1964, there is no blanket prohibition on government servants investing in mutual funds, including through SIPs. However, there are important conditions:

In practice, government employees investing in mutual funds via SIPs for long-term goals such as children’s education, supplementary retirement income, or wealth creation is widely accepted, provided it is done transparently and within prescribed limits. For NPS subscribers, equity exposure is already built in through NPS Tier I. Mutual funds offer an additional avenue for those seeking higher long-term returns.

Practical guidance: If you are unsure whether a specific mutual fund investment requires prior intimation, consult your department’s vigilance or administrative section, or seek advice from a certified financial planner.

Despite CGHS and the Fixed Medical Allowance, coverage gaps remain, particularly in cities without CGHS empanelment and for treatments not covered under CGHS. A top-up health policy of ₹10-25 lakh is recommended for all government retirees.

Proactive action in the five years before retirement can significantly improve your financial outcome.

The landscape of retirement planning for government employees in India has never been more dynamic than it is in 2026. The Unified Pension Scheme is fully operational. Fixed Medical Allowance is now aligned across pension schemes. The General Provident Fund interest rate holds steady at 7.1%. And leave encashment rules continue to offer a complete tax exemption at retirement for government employees.

But no benefit, however well designed, replaces a personalized retirement plan, one that accounts for your service period, chosen pension scheme, family requirements, and post-retirement income goals.

Whether you are 10 years from retirement or 10 months away, the decisions you make today, verifying your service record, reviewing your NPS vs Unified Pension Scheme choice, using your retirement benefits for government employees wisely, and building supplementary income, will define your financial security for decades to come.

Talk to us

Investor Grievance

Talk to us

Investor Grievance