Every taxpayer in India must choose between two tax regimes before filing an income tax return: the old regime and the new regime. The new regime is now the default option for most individuals, HUFs, AOPs and BOIs. This means if you do nothing, your tax will be calculated under the new regime. If the old regime works out better for you, you have to actively choose it while filing.

| Point | Old Tax Regime | New Tax Regime |

|---|---|---|

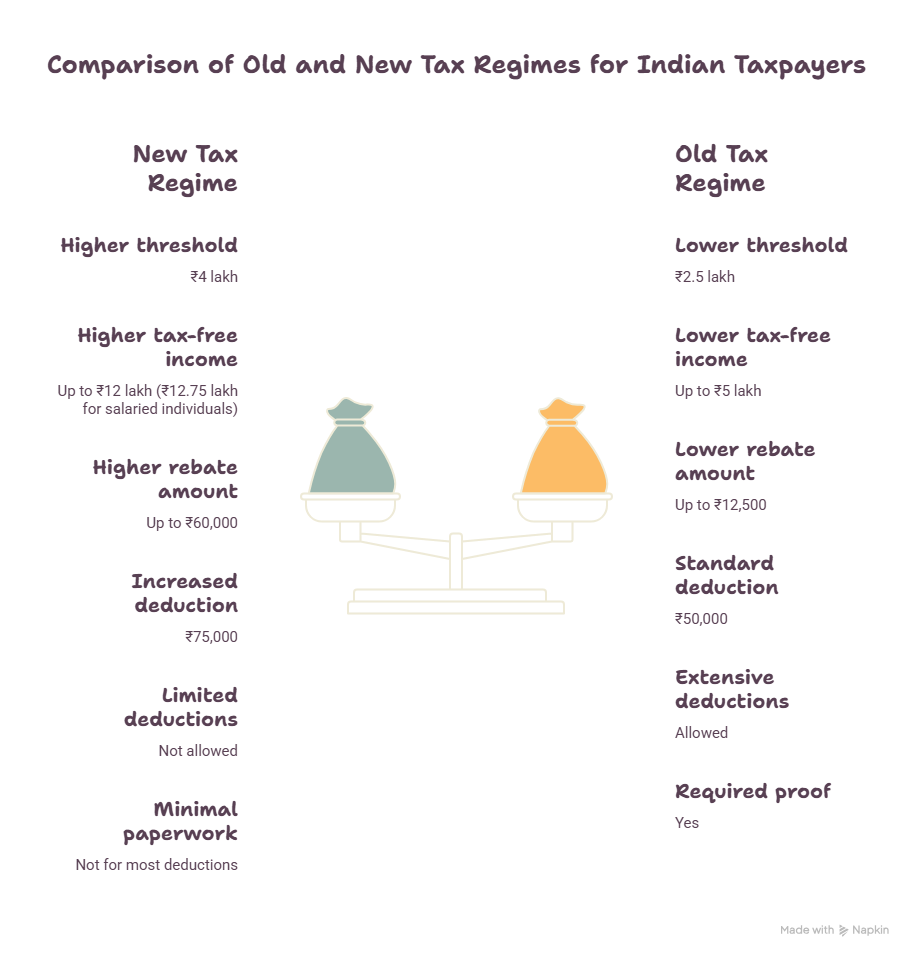

| Basic exemption limit | ₹2.5 lakh | ₹4 lakh |

| Income that is effectively tax-free | Up to ₹5 lakh | Up to ₹12 lakh (₹12.75 lakh for salaried individuals) |

| Section 87A rebate | Up to ₹12,500 | Up to ₹60,000 |

| Standard deduction | ₹50,000 | ₹75,000 |

| HRA, LTA, 80C, 80D, home loan interest on self-occupied property | Allowed | Not allowed |

| Default regime for FY 2025-26 | No, must be selected | Yes |

| Proof of investments needed | Yes | Not for most deductions |

The old regime allows various deductions and exemptions, while the new regime offers lower tax rates but permits only limited deductions and exemptions. There is no single answer for which regime is better. It depends on comparing both, done individually for each taxpayer.

For individuals below 60 years of age, the old regime slabs are as follows:

| Income | Tax Rate |

|---|---|

| Up to ₹2.5 lakh | Nil |

| ₹2.5 lakh to ₹5 lakh | 5% |

| ₹5 lakh to ₹10 lakh | 20% |

| Above ₹10 lakh | 30% |

Senior citizens (60 to 80 years) get a higher basic exemption limit of ₹3 lakh, and super senior citizens (above 80 years) get ₹5 lakh, under the old regime.

No tax is payable on income up to ₹12 lakh, except for income taxed at special rates, such as capital gains. For salaried taxpayers, this limit increases to ₹12.75 lakh due to the ₹75,000 standard deduction.

| Income | Tax Rate |

|---|---|

| Up to ₹4 lakh | Nil |

| ₹4 lakh to ₹8 lakh | 5% |

| ₹8 lakh to ₹12 lakh | 10% |

| ₹12 lakh to ₹16 lakh | 15% |

| ₹16 lakh to ₹20 lakh | 20% |

| ₹20 lakh to ₹24 lakh | 25% |

| Above ₹24 lakh | 30% |

This slab structure applies the same way regardless of age. Unlike the old regime, the new regime does not give senior citizens a higher basic exemption limit.

An exemption is a portion of your income that is excluded from the tax calculation altogether, such as an allowance. HRA exemption under Section 10(13A) is not available in the new regime. Interest paid on a home loan for a self-occupied property is also not allowed as a deduction from income under the new regime.

A limited set of allowances and exemptions do continue to apply in the new regime:

A deduction reduces your taxable income based on an eligible expense or contribution, unlike an exemption which excludes income outright. The list of new tax regime deductions allowed is short compared to the old regime:

Deductions available in the new tax regime do not include Section 80C, Section 80D, Section 80E, Section 80G, or most other deductions listed under Chapter VI-A. If a deduction is not on the short list above, it is generally unavailable under the new regime.

The standard deduction in the new regime is ₹75,000 for salaried individuals and pensioners for FY 2025-26. This is higher than the ₹50,000 standard deduction available under the old regime. A standard deduction of ₹50,000, or the salary amount if lower, has been available in both regimes from AY 2024-25 onwards, and was later raised to ₹75,000 for the new regime.

This deduction is applied automatically against salary income. You do not need to submit any proof or make any investment to claim it, in either regime.

No. Section 80C, which covers investments such as EPF, PPF, ELSS, life insurance premiums, and principal repayment on a home loan, is not available under the new tax regime. This deduction, along with Section 80D (health insurance premium), Section 80E (education loan interest) and most other Chapter VI-A deductions, applies only if you file under the old regime.

If you have made 80C investments during the year and want to claim them, you need to select the old regime while filing your return.

The old tax regime allows a wide range of deductions under Chapter VI-A of the Income Tax Act. The commonly used ones include:

Claiming these deductions requires supporting documents, such as proof of investment, rent receipts, and loan interest certificates, which need to be maintained and, in some cases, submitted to your employer or kept ready in case of a tax department query.

The main benefit of the new regime is a lower tax outgo for individuals who do not have large deductions to claim. Because of the ₹60,000 rebate under Section 87A and the ₹75,000 standard deduction, salaried individuals with an income up to ₹12.75 lakh pay no tax under the new regime.

Other benefits include:

The choice between the old and new tax regime comes down to how much you can claim under Chapter VI-A deductions and exemptions, such as HRA and home loan interest. If your eligible deductions are small, the new regime’s lower slab rates and higher rebate usually work out cheaper. If you have a home loan, pay rent, or invest heavily in 80C and 80D instruments, the old regime may still save you more. The only reliable way to know is to work out your tax under both regimes with your actual numbers before you file, check which regime your ITR form has selected by default, and confirm you have the proof ready for any deduction you plan to claim.

Talk to us

Investor Grievance

Talk to us

Investor Grievance