A practical, step-by-step guide to building a retirement plan that protects your income, your health, and everything you’ve worked hard to enjoy.

Retirement is supposed to be the reward at the end of a lifetime of hard work. Yet for millions of people, it arrives with an unexpected concern: financial anxiety. The fear of running out of money, scaling back hobbies, or giving up the lifestyle you’ve built can make retirement feel less like a celebration and more like a difficult transition.

The good news? With the right retirement planning approach, you don’t have to choose between financial security and living well. This guide shows you exactly how to retire without compromising your lifestyle, whether you’re 10 years away or already transitioning.

Before diving into steps, let’s ground this in reality. The biggest mistake most people make in retirement planning is underestimating what they’ll actually spend.

Many advisors still recommend the outdated “70–80% of pre-retirement income” rule. But research consistently shows that active retirees in their 60s often spend as much as, or more than, they did while working, especially in the early years, often called the Go-Go Years.

Note: Track your current monthly spending in detail for 3–6 months before retiring. This gives you a real baseline, not a guess.

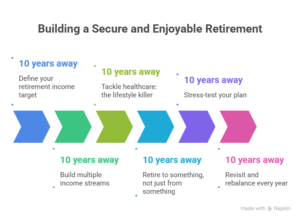

Retirement income planning starts with a concrete number. Use this simple framework rooted in the widely studied 4% Rule:

Annual Lifestyle Cost × 25 = Your Retirement Savings Target

If your ideal retirement lifestyle costs ₹80,000 per month (₹9.6L per year), your savings target would be approximately ₹2.4 crore. Most financial planners recommend building in a buffer of 10–20% above your baseline to account for inflation, market swings, and healthcare surprises.

Relying on a single income source in retirement is one of the most common and costly mistakes. A lifestyle-sustaining retirement income plan draws from multiple pillars:

Whether it’s Social Security, EPF/NPS, or a public sector pension, understanding exactly what you’re entitled to and the best time to claim can dramatically affect your monthly income. Delaying claims often significantly increases your benefit.

A well-balanced retirement portfolio should include equities for growth, bonds for stability, and liquid assets for short-term needs. Many retirees use a “bucket strategy”, dividing assets into short-term (1–3 years), medium-term (4–10 years), and long-term (10+ years) buckets to manage volatility without panic-selling.

Passive income for retirement is increasingly important. Consider rental income from real estate, dividend-paying stocks, REITs, annuities, or royalties. Even modest passive income of ₹20,000–₹30,000 per month can significantly reduce the drawdown pressure on your core portfolio.

Many early retirees find joy and income in passion-based work, consulting in their field, freelancing, or turning hobbies into revenue. Studies show that purposeful part-time engagement improves retirement satisfaction and cognitive health.

Healthcare is the single biggest threat to a comfortable retirement. A major health event without adequate coverage can wipe out decades of savings. This is non-negotiable in any conversation about retirement lifestyle planning.

Financial security is only half the retirement equation. Research in positive psychology consistently shows that purpose, social connection, and routine are as critical to retirement satisfaction as financial stability.

Retirees who maintain a high quality of life tend to have clear goals and meaningful activities, stay socially connected through community or travel groups, continue learning through courses or workshops, and prioritize preventive health and physical activity.

Retirement lifestyle planning isn’t just a spreadsheet exercise; it’s a design challenge. Treat your retirement like a life you’re intentionally building.

Even the best retirement income planning can be disrupted by unexpected events. Before you retire, model your plan against:

Monte Carlo simulations and consultations with a certified financial planner (CFP) can help you model these scenarios and adjust accordingly.

A retirement plan is not a “set it and forget it” document. Build an annual review into your routine, rebalance your portfolio, reassess your withdrawal rate, update your estate plan, and review insurance coverage as your life evolves.

Retiring without compromising your lifestyle isn’t a pipe dream reserved for the ultra-wealthy; it’s the outcome of intentional planning, smart income diversification, and a clear-eyed view of what your life actually costs.

The six steps in this guide aren’t a checklist to rush through. They’re a framework to return to again and again as your circumstances evolve. Start with the number that defines your lifestyle. Build the income pillars to support it. Protect yourself against healthcare risk. And invest just as much energy into designing a purposeful post-work life as you do into your financial portfolio.

The best time to start was yesterday. The second-best time is today.

Not sure where you stand? Check your Retirement Readiness Score and find out how prepared you really are.

Talk to us

Investor Grievance

Talk to us

Investor Grievance