Rebalancing frequency optimization is a critical aspect of portfolio management that can significantly impact investment performance and risk management. By strategically adjusting the frequency at which a portfolio is rebalanced, investors can maintain their desired asset allocation while potentially enhancing returns and minimizing costs. This article examines the details of optimizing rebalancing frequency and its importance in modern investment strategies.

Rebalancing frequency optimization refers to the process of determining the ideal intervals at which to realign a portfolio’s asset allocation with its target composition. This practice is essential for maintaining the intended risk-return profile of an investment strategy over time. As market fluctuations cause certain assets to outperform or underperform, the portfolio’s composition can drift away from its original allocation, potentially exposing investors to unintended risks or missed opportunities.

The frequency of rebalancing can have a significant impact on a portfolio’s long-term performance. Too frequent rebalancing may result in unnecessary transaction costs and tax implications, while infrequent rebalancing can lead to prolonged periods of misalignment with the target allocation. Finding the optimal balance between these extremes is crucial for maximizing risk-adjusted returns and achieving investment objectives.

The level of market volatility plays a crucial role in determining the optimal rebalancing frequency. During periods of high volatility, such as those experienced during major economic events or crises, more frequent rebalancing may be necessary to maintain the desired asset allocation. Conversely, in calmer market conditions, less frequent rebalancing may suffice.

An investor’s specific goals and time horizon significantly influence the appropriate rebalancing frequency. Long-term investors may opt for less frequent rebalancing, while those with shorter time horizons or more specific near-term objectives might require more regular portfolio adjustments.

The costs associated with rebalancing, including brokerage fees and potential tax implications, must be carefully considered when optimizing rebalancing frequency. These expenses can erode returns if rebalancing is performed too frequently, especially in taxable accounts where capital gains taxes may be triggered.

An investor’s risk tolerance is a crucial factor in determining the optimal rebalancing frequency. Those with lower risk tolerance may prefer more frequent rebalancing to ensure their portfolio remains closely aligned with their target allocation, while investors with higher risk tolerance might be comfortable with less frequent adjustments.

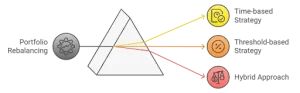

Time-based rebalancing involves adjusting the portfolio at predetermined intervals, such as quarterly, semi-annually, or annually. This approach provides consistency and discipline but may not always align with market conditions or portfolio drift.

Threshold-based rebalancing triggers portfolio adjustments when asset allocations deviate from their targets by a specified percentage. This method is more responsive to market movements but may result in more frequent trading during volatile periods.

Many investors and financial advisors opt for hybrid approaches that combine elements of time-based and threshold-based strategies. For example, a portfolio might be reviewed quarterly but only rebalanced if allocations have drifted beyond predetermined thresholds.

Examining historical market data and portfolio performance can provide valuable insights into optimal rebalancing frequencies. By analyzing how different rebalancing strategies would have performed in various market conditions, investors can make more informed decisions about their approach.

Backtesting involves simulating the performance of various rebalancing strategies using historical data. This process can help identify which approaches would have produced the best results over different time periods and market cycles.

When optimizing rebalancing frequency, it’s essential to consider risk-adjusted returns rather than focusing solely on absolute performance. Metrics such as the Sharpe ratio or Sortino ratio can provide a more comprehensive view of a strategy’s effectiveness in balancing risk and reward.

Advanced portfolio management software can automate much of the rebalancing process, making it easier to implement and monitor complex strategies.

Robo-advisors have gained popularity in recent years, offering automated rebalancing services based on predetermined rules and algorithms. These platforms can provide cost-effective solutions for investors seeking professional portfolio management.

For high-net-worth individuals and institutional investors, professional advisory services can offer customized rebalancing strategies tailored to specific investment goals and risk profiles. These services often leverage sophisticated tools and expertise to optimize rebalancing frequency and execution.

Establishing clear, well-defined rules for rebalancing is crucial for successful implementation. These rules should specify triggers for rebalancing, target allocation ranges, and any constraints or considerations specific to the investor’s situation.

Regular monitoring of the portfolio and the effectiveness of the rebalancing strategy is essential. As market conditions change or investment goals evolve, it may be necessary to adjust the rebalancing approach to ensure it remains optimal.

Maintaining detailed records of rebalancing decisions and their outcomes can provide valuable insights for future optimization. This documentation can also be helpful for compliance purposes and performance evaluation.

Investors must be aware of behavioral biases that can impact rebalancing decisions, such as the reluctance to sell winning positions or the tendency to hold onto losing investments. Adhering to a systematic rebalancing strategy can help mitigate these biases.

While rebalancing is not intended as a market timing tool, the timing of rebalancing actions can inadvertently impact returns. It’s important to strike a balance between maintaining the target allocation and avoiding excessive trading based on short-term market movements.

The potential benefits of rebalancing must always be weighed against the associated costs. In some cases, the transaction costs and tax implications of rebalancing may outweigh the benefits of minor allocation adjustments.

Artificial intelligence and machine learning algorithms are increasingly being applied to portfolio rebalancing, offering the potential for more sophisticated and responsive strategies that can adapt to changing market conditions in real-time.

As financial planning becomes more holistic, rebalancing strategies are likely to become more integrated with other aspects of an investor’s financial life, such as tax planning, retirement savings, and estate planning.

Advancements in technology and data analytics are enabling more personalized rebalancing strategies that can account for an individual investor’s unique circumstances, preferences, and goals.

In conclusion, rebalancing frequency optimization is a critical component of successful portfolio management. By carefully considering factors such as market conditions, investment goals, and costs, investors can develop and implement rebalancing strategies that help maintain their desired asset allocation while potentially enhancing long-term performance. As technology continues to evolve, the tools and techniques available for optimizing rebalancing frequency are likely to become even more sophisticated, offering new opportunities for investors to fine-tune their approach to rebalancing frequency optimization.

For investors looking to improve their portfolio management strategies, including optimizing rebalancing frequency, consider exploring the wealth management services offered by financial professionals who can provide personalized advice and implement sophisticated rebalancing strategies tailored to your specific needs and goals.

Talk to us

Investor Grievance

Talk to us

Investor Grievance