Pension plans in India are long-term savings instruments that build a retirement corpus during your working years and convert it into regular income after you stop working. In 2026, the National Pension System remains the backbone of India’s market-linked pension architecture, with significant PFRDA reforms on withdrawals, equity allocation and eligibility age that every investor needs to know before choosing a plan.

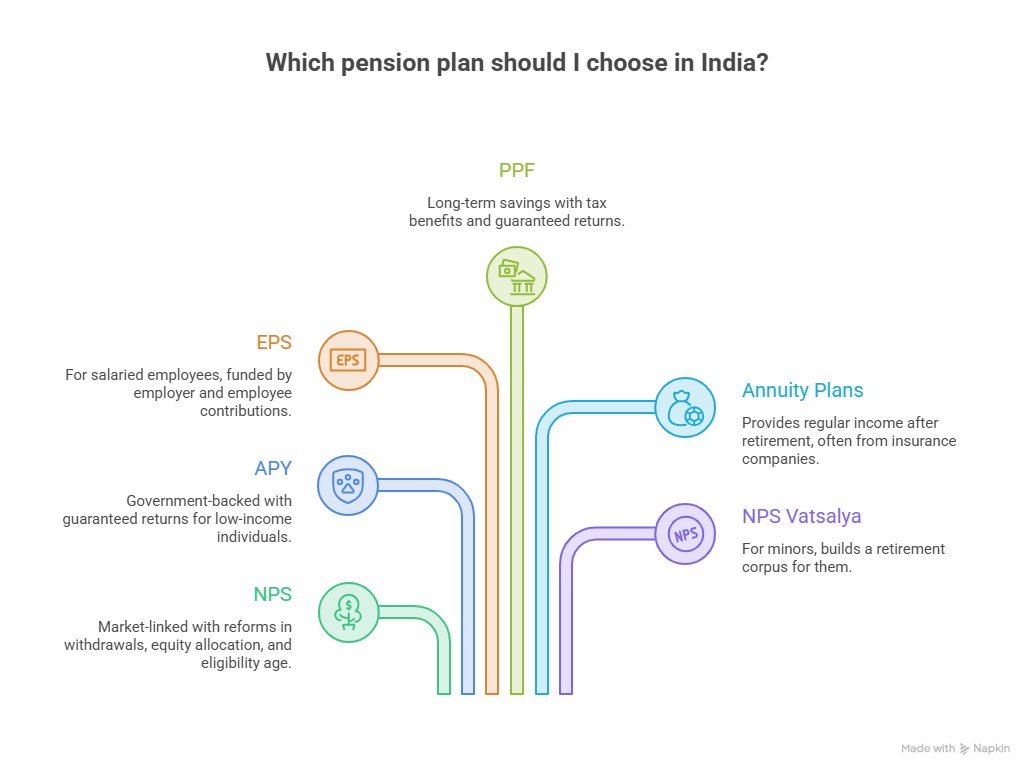

India’s pension landscape in 2026 covers six major categories: NPS, Atal Pension Yojana, EPS, PPF, insurance annuity plans and NPS Vatsalya for minors. Each is designed for a different segment of the population, so the right combination depends on your employment type, income, risk appetite and years remaining until retirement.

The National Pension System is a market-linked, defined-contribution scheme regulated by the PFRDA and open to all Indian citizens aged 18 to 70. Subscribers choose their fund manager and allocate across equity, corporate bonds and government securities. The NPS corpus at retirement can be partially withdrawn as a lump sum, with the remainder used to buy an annuity for regular pension income.

Atal Pension Yojana is aimed at workers in the unorganised sector and offers a guaranteed monthly pension of between Rs 1,000 and Rs 5,000 after age 60, depending on the contribution amount and the age at which contributions begin. APY is one of the few schemes in India’s pension landscape that provides a fully guaranteed payout, with the government underwriting the pension obligation.

EPS pension is a mandatory component of the EPFO framework for organised-sector employees. A portion of the employer’s provident fund contribution is directed to EPS each month, and the eventual monthly EPS pension depends on the pensionable salary and years of contributory service.

The Public Provident Fund is a government-backed, long-term savings scheme open to all resident Indian individuals, including salaried employees, self-employed professionals and homemakers. It is not a pension plan in the strict sense, but its structure — a 15-year lock-in with partial withdrawal provisions, tax-free interest and an EEE (Exempt-Exempt-Exempt) tax status — makes it one of the most effective guaranteed-return instruments for building a retirement corpus.

Key features of PPF in 2026:

PPF as a retirement tool: For investors who want zero-risk, tax-free compounding over 15 to 25 years, PPF is an excellent complement to NPS. While NPS provides market-linked growth and a regular annuity in retirement, PPF accumulates a guaranteed lump sum that can be withdrawn tax-free at maturity or extended to continue compounding. Together, they address both the growth and the capital-preservation requirements of a retirement portfolio.

Private-sector annuity plans in India allow individuals to either accumulate a corpus over a policy term or convert a lump sum into immediate regular income. Deferred annuity plans build the corpus first, while immediate annuity plans start paying from month one. Joint-life annuity plans continue payments to a surviving spouse, making them a useful income protection tool for households.

NPS Vatsalya allows parents or guardians to open an NPS account in a minor’s name. On turning 18, the account converts to a standard NPS account in the child’s name, providing an early accumulation runway and access to the same tax treatment as regular NPS contributions.

The PFRDA introduced several meaningful reforms to the National Pension System between late 2025 and early 2026 that expand flexibility for subscribers. The key updates are:

Budget 2026 did not introduce new NPS tax deductions or contribution changes. Section 80CCD deductions, including the additional Rs 50,000 under Section 80CCD(1B), remain unchanged.

| Feature | NPS | Atal Pension Yojana | EPS | PPF | Annuity Plans |

|---|---|---|---|---|---|

| Who can join | All citizens (18–70) | Unorganised sector workers | Organised-sector EPFO employees | All resident individuals | Anyone with a lump sum |

| Returns | Market-linked | Government-guaranteed | Formula-based | Government-fixed (7.1% p.a.) | Locked-in rate at purchase |

| Payout type | Lump sum (up to 80%) + annuity | Fixed monthly pension | Monthly EPS pension | Lump sum at maturity | Regular income (monthly/quarterly) |

| Tax benefit | Section 80CCD | Section 80C (via bank contributions) | No separate deduction | Section 80C; interest & maturity tax-free (EEE) | No deduction |

| Flexibility | High | Low | Employer-linked | Moderate (partial withdrawals from year 7) | Moderate |

| Market risk | Yes | No | No | No | No |

| Regulator | PFRDA | Government of India | EPFO | Ministry of Finance | IRDAI |

NPS suits investors looking for market-linked growth and flexible corpus management; Atal Pension Yojana suits those who want a guaranteed floor income with minimal decision-making. NPS 2026 reforms make it increasingly versatile for working professionals who want to control their equity-debt mix, while APY remains the more straightforward option for self-employed individuals or gig workers without access to employer pension contributions.

For those who want to combine both, holding APY as a guaranteed-income floor alongside an NPS account for growth-linked retirement accumulation is a common approach among individuals who split their time between salaried and self-employed work.

Self-employed individuals can open an NPS Tier I account voluntarily and access the same Section 80CCD deductions available to salaried subscribers. There is no employer contribution component for the self-employed, but the National Pension System’s low fund management charges and the newly removed five-year lock-in under the All Citizen Model make it a practical standalone retirement tool.

PPF is equally well-suited for the self-employed. Since there is no employer involved, a PPF account opened at a post office or bank gives self-employed individuals a disciplined, tax-efficient savings channel that is fully independent of employment status. The annual contribution ceiling of Rs 1.5 lakh fits neatly within the Section 80C limit, and the guaranteed, tax-free interest makes it a stable counterweight to the market-linked volatility of NPS.

Combining NPS with PPF, voluntary provident fund and annuity plans in India can create a layered retirement portfolio with both growth and guaranteed income streams.

If you are in formal employment under EPFO, EPS pension is mandatory, and NPS may be available as an additional tier through your employer. If you are self-employed or in the gig economy, NPS, PPF and Atal Pension Yojana are the three most direct options — each serving a different purpose in the retirement portfolio.

The annuity portion of your NPS corpus and the eventual EPS pension are separate income streams that work differently in retirement. PPF, by contrast, delivers a lump sum at maturity that you can redeploy into an immediate annuity or keep growing through block extensions. Thinking about how much guaranteed monthly income you need (from APY, EPS or annuity plans) versus how much you want as a flexible lump sum (from NPS or PPF) helps structure the right combination.

With the National Pension System now allowing up to 100% equity allocation for non-government subscribers, it is worth revisiting your NPS fund mix as your risk appetite and years to retirement change. Staying in the default auto-choice without reviewing it can leave potential growth on the table in the early years and insufficient protection in the years closer to retirement.

Pension plans in India work best as one layer of a broader retirement strategy. A practical framework for most individuals looks like this:

Reviewing your overall asset allocation periodically, especially after the 2025-26 NPS reforms, helps keep your retirement planning in India aligned with your evolving goals. At Right Horizons, our team can help you structure the right combination of pension plans, PPF, annuity plans and other retirement assets based on your situation. Explore our financial planning services or speak with our team about your retirement planning goals today.

Talk to us

Investor Grievance

Talk to us

Investor Grievance