Investment Options for Retirees: Ensuring Financial Stability in Retirement

Key Points

- Balancing income generation and capital preservation through diversification is essential for retirees

- Government-backed schemes like SCSS and PMVVY provide secure, tax-efficient investment options

- Expert financial guidance can help create personalized investment strategies based on individual needs and risk tolerance

- Regular portfolio assessments and adjustments are necessary to maintain financial stability throughout retirement

- Tax planning is a vital element of retirement investment strategies

Investing for retirement is crucial for maintaining financial stability and tranquility during one’s later years. As individuals transition from their careers to retirement, the focus shifts from accumulating wealth to preserving it and generating consistent income. This guide explores various investment avenues tailored to meet the specific needs of retirees in India, offering insights into strategies that balance security, returns, and tax efficiency.

Understanding Investment Requirements in Retirement

Retirement brings about a significant change in financial priorities. The main objectives for retirees typically include:

- Creating regular income to cover living expenses

- Maintaining capital to ensure long-term financial security

- Addressing inflation risk to maintain purchasing power

- Reducing tax liability to optimize returns

To achieve these goals, retirees must carefully evaluate their risk tolerance, financial objectives, and time horizon. This assessment forms the basis for developing a robust investment strategy that aligns with their unique circumstances.

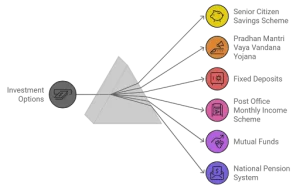

Overview of Investment Options for Retirees

1. Senior Citizen Savings Scheme (SCSS)

The SCSS is a government-backed savings scheme designed specifically for senior citizens. Key features include:

- Eligibility: Individuals aged 60 years and above

- Interest rate: Currently offering 8.2% per annum (subject to change)

- Investment limit: Up to ₹15 lakhs

- Tenure: 5 years, extendable by 3 years

- Tax benefits: Interest income is taxable, but eligible for deduction under Section 80TTB

2. Pradhan Mantri Vaya Vandana Yojana (PMVVY)

PMVVY is another government-sponsored scheme aimed at providing social security to senior citizens. Notable aspects include:

- Eligibility: Individuals aged 60 years and above

- Interest rate: 7.4% per annum (fixed for the entire policy term)

- Investment limit: Up to ₹15 lakhs

- Tenure: 10 years

- Payout options: Monthly, quarterly, half-yearly, or annually

3. Fixed Deposits (FD)

Bank fixed deposits remain a popular choice among retirees due to their simplicity and perceived safety. Key points to consider:

- Interest rates: Vary across banks, with some offering higher rates for senior citizens

- Tenure: Flexible options ranging from 7 days to 10 years

- Liquidity: Early withdrawal allowed with penalty

- Tax implications: Interest income is fully taxable

4. Post Office Monthly Income Scheme (POMIS)

POMIS offers a reliable monthly income option for retirees. Important features include:

- Investment limit: Up to ₹4.5 lakhs for single account, ₹9 lakhs for joint account

- Interest rate: Currently 7.1% per annum (paid monthly)

- Tenure: 5 years

- Tax status: Interest income is fully taxable

5. Mutual Funds

Mutual funds offer diversification and professional management, making them an attractive option for retirees. Key considerations include:

- Types: Debt funds, balanced funds, and equity funds (including ELSS)

- Risk profile: Varies based on the fund type and investment strategy

- Returns: Potential for higher returns compared to fixed-income options

- Tax efficiency: Long-term capital gains taxed at 10% above ₹1 lakh for equity funds

6. National Pension System (NPS)

While primarily designed for long-term retirement savings, NPS can also be utilized by retirees. Notable aspects include:

- Contribution limit: No upper limit

- Investment options: Choice of asset allocation between equity and debt

- Tax benefits: Additional tax deduction of up to ₹50,000 under Section 80CCD(1B)

- Partial withdrawal: Allowed for specific purposes after 3 years

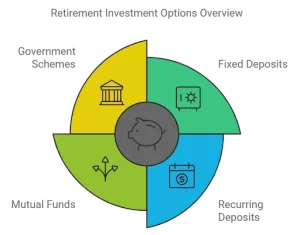

Detailed Analysis of Investment Options

Fixed Deposits and Recurring Deposits

Fixed deposits offer stability and predictable returns, making them a cornerstone of many retirees’ portfolios. Benefits include:

- Guaranteed returns

- Flexible tenure options

- Special rates for senior citizens

However, drawbacks include:

- Fully taxable interest income

- Lower returns compared to some other options

- Potential for negative real returns in high-inflation scenarios

Bank FDs can be complemented with recurring deposits to build a ladder of maturity dates, ensuring regular liquidity while maximizing overall returns.

Mutual Funds

Mutual funds provide an excellent avenue for retirees to achieve diversification and potentially higher returns. Key points to consider:

- Debt funds: Offer stability and regular income, suitable for conservative investors

- Balanced funds: Provide a mix of equity and debt, balancing growth and income

- Equity funds: Offer potential for capital appreciation, but with higher risk

Retirees should carefully assess their risk tolerance and investment horizon when selecting mutual funds. Systematic Withdrawal Plans (SWPs) can be utilized to generate regular income from mutual fund investments.

Government Schemes

Government-backed schemes like SCSS and PMVVY offer a combination of safety, attractive returns, and tax benefits. These schemes are particularly suitable for risk-averse retirees seeking guaranteed income. Key advantages include:

- Higher interest rates compared to bank FDs

- Government backing ensures capital safety

- Tax benefits under various sections of the Income Tax Act

However, investment limits and fixed tenures may necessitate combining these schemes with other investment options for a comprehensive portfolio.

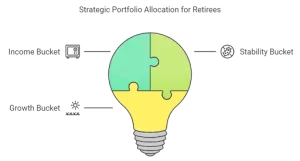

Strategies for Portfolio Allocation

Effective portfolio allocation is crucial for retirees to balance income generation, capital preservation, and growth. Consider the following strategies:

- Income Bucket: Allocate 2-3 years of expenses to highly liquid, low-risk options like bank FDs and liquid funds.

- Stability Bucket: Invest 3-5 years of expenses in government schemes, debt funds, and high-quality corporate bonds.

- Growth Bucket: Allocate remaining funds to a mix of equity mutual funds and balanced funds for long-term growth.

The exact allocation percentages should be tailored to individual risk tolerance and financial goals. Regular portfolio rebalancing is essential to maintain the desired asset allocation over time.

Tax Considerations for Retirees

Tax planning is a critical aspect of retirement investment strategy. Key considerations include:

- Utilize tax-saving investments like ELSS funds to reduce tax liability

- Leverage tax benefits under Section 80TTB for interest income

- Optimize withdrawals to minimize overall tax impact

- Consider tax-efficient debt mutual funds for fixed-income allocation

Consulting with a tax professional can help retirees navigate complex tax laws and maximize their after-tax returns.

Importance of Professional Financial Advice

Given the complexity of retirement planning and the multitude of investment options available, seeking professional financial advice can be invaluable. A qualified financial advisor can:

- Assess individual financial situations and goals

- Develop a customized investment strategy

- Provide guidance on tax-efficient investment options

- Assist with regular portfolio reviews and rebalancing

When selecting a financial advisor, look for credentials, experience, and a fiduciary commitment to act in your best interests.

Summary

Investment options for retirees in India offer a diverse range of opportunities to ensure financial stability and peace of mind during retirement. By carefully assessing individual needs, risk tolerance, and financial goals, retirees can create a well-balanced portfolio that provides regular income, preserves capital, and offers potential for growth. The key to successful retirement planning lies in diversification, regular reviews, and seeking professional advice when needed. With the right approach, retirees can confidently navigate their financial journey and enjoy a comfortable and secure retirement.

Talk to us

Talk to us