Sovereign Gold Bonds (SGBs) are government-backed securities denominated in grams of gold, issued by the RBI on behalf of the Government of India. In 2026, no new SGB tranche is available for subscription. Investors who want to buy Sovereign Gold Bonds today can only do so through the secondary market on the NSE or BSE using a demat account, while existing holders follow the RBI’s SGB redemption calendar to exit their positions.

Sovereign Gold Bonds are paper-based gold investment instruments, first introduced in November 2015 as an alternative to physical gold. Each SGB is denominated in grams and pays a fixed interest of 2.5% per annum, credited semi-annually, on top of any appreciation in gold prices over the holding period. The bonds carry a tenure of eight years with an option for premature redemption after the fifth year, on specific interest payment dates.

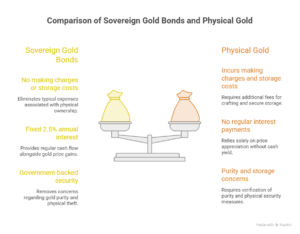

Because SGBs are backed by the Government of India and the Sovereign Gold Bond interest rate is fixed at 2.5%, they remain one of the few gold investment instruments that generate a regular cash flow alongside gold price gains. There are no making charges, storage costs or purity concerns, which are typical drawbacks of physical gold.

The government confirmed that no new SGB portion would be issued after the 2023-24 Series IV, citing the high cost of servicing the scheme against a backdrop of rising gold prices. As of June 2026, the RBI has not released any SGB issuance calendar for FY 2026-27. This means new investors cannot subscribe to a fresh tranche at the government-declared issue price and must instead look at the secondary market.

In 2026, the only way to buy Sovereign Gold Bonds is through the NSE or BSE secondary market using an active demat and trading account. The process is straightforward but involves a few steps that differ from original subscription.

| Step | What You Need to Do |

|---|---|

| Step 1: Open or Use an Existing Demat and Trading Account | All outstanding SGB series are listed on the NSE and BSE. You need an active demat and trading account with a registered broker, similar to how you would buy shares. |

| Step 2: Search for the Right SGB Series | Each SGB series trades under its own ticker, such as SGBOCT26 or SGBAUG28. Series vary by residual tenure, the number of interest payments remaining and prevailing market price. |

| Step 3: Compare the Market Price Against the Gold Rate | Secondary market SGB prices can trade at a premium or discount to the prevailing gold rate, depending on demand, liquidity and the coupon remaining. Before you buy Sovereign Gold Bonds on the exchange, compare the quoted price with the current gold price to assess value. |

| Step 4: Place Your Order and Hold in Demat Form | Once purchased, the bonds sit in your demat account like any security. You continue to receive the 2.5% Sovereign Gold Bond interest rate as long as you hold, and redemption at maturity or during an eligible premature redemption window is processed by the RBI at the prevailing gold rate. |

| Feature | Sovereign Gold Bond | Gold ETF | Digital Gold |

|---|---|---|---|

| Fixed interest | 2.5% p.a. | None | None |

| New availability | Secondary market only | Always available | Always available |

| Tax at maturity original holder | Exempt | Capital gains tax | Capital gains tax |

| Tax at maturity secondary buyer | Capital gains tax from Apr 2026 | Capital gains tax | Capital gains tax |

| Storage risk | None | None | Platform-dependent |

| Expense ratio | None | 0.1% to 0.5% | Spread on buy/sell |

| Regulated by | RBI / GoI | SEBI | Unregulated |

| Minimum investment | 1 gram | 1 unit approx. 1 gram | As low as ₹1 |

The gold ETF vs SGB comparison now depends more on the secondary-market premium and the post-tax return than it did when fresh SGBs were available. For investors who already hold SGBs, the 2.5% coupon and, for original holders, the tax exemption at maturity remain distinct advantages that neither gold ETFs nor digital gold can replicate.

SGB redemption works through the RBI’s premature redemption calendar, which lists eligible portions every six months. Investors in Portion issued between 2018-19 and 2021-22 are progressively reaching their five-year mark through 2026, making April, July and August particularly active SGB redemption months.

To redeem early, submit a request through the bank, post office, depository participant or SHCIL within the window specified for that tranche. The SGB redemption price is based on the simple average closing price of 999-purity gold published by IBJA for the three business days preceding the redemption date. At full maturity after eight years, redemption is automatic and proceeds are credited to the registered bank account.

Sovereign Gold Bonds were originally restricted to resident Indian entities, including individuals, HUFs, trusts, universities and charitable institutions. If you already hold SGBs and your residential status changes to non-resident, you may continue to hold until maturity or an eligible SGB redemption window, subject to FEMA rules. New buyers in the secondary market need to meet standard KYC norms applicable to demat accounts, including PAN, Aadhaar and a linked bank account.

From 1 April 2026, the capital gains tax exemption on SGBs at redemption applies only to original subscribers who held continuously from issue date to maturity. Previously, any investor redeeming an SGB at maturity was exempt from capital gains tax on gold price appreciation. The SGB tax change introduced in Budget 2026 means investors who buy SGBs from the secondary market and hold them to redemption are now liable for capital gains tax on the appreciation.

The 2.5% annual interest continues to be taxed as “Income from Other Sources” at the investor’s slab rate, with no TDS deducted and no Section 80C deduction on the investment amount. This SGB tax shift makes it important to factor in the post-tax return before buying on the exchange, particularly for investors in higher tax brackets.

To redeem an SGB, you need your demat or bond certificate details, a filled redemption request form, a linked bank account for credit and a valid identity proof such as PAN. The exact set of documents varies slightly depending on whether the bond is held in demat form, as a certificate of holding, or through a bank or post office, but the following are required across all channels:

| Document | Purpose | Where Applicable |

|---|---|---|

| SGB Certificate of Holding / Demat statement | Proof of bond ownership and series details | All holders |

| Redemption request form | Formal request to trigger premature or maturity redemption | All holders |

| PAN card | KYC and tax compliance | All holders |

| Aadhaar card | Identity verification | All holders |

| Bank account details cancelled cheque or passbook copy | For crediting redemption proceeds | All holders |

| Original bond certificate if in physical form | Surrender at the time of redemption | Physical certificate holders only |

Redemption requests must be submitted through the same channel used for the original subscription, which could be a bank, post office, SHCIL, registered broker or depository participant. For demat-held SGBs, the request is typically initiated online through the broker or depository interface. The RBI processes the request and credits the redemption amount, calculated at the prevailing IBJA gold price, directly to the registered bank account within the prescribed timelines.

| Common Mistake | Why It Matters |

|---|---|

| Assuming SGBs Are Still Tax-Free for All Holders | One of the most common misconceptions is that all SGBs remain tax-free at redemption. The 2026 SGB tax change only protects original subscribers, not secondary market buyers. |

| Ignoring the Premium Over Spot Gold | Secondary market SGB prices often trade at a premium to the live gold rate. Paying a significant premium can dilute the benefit of the 2.5% Sovereign Gold Bond interest rate, so comparing prices across series is important. |

| Missing the SGB Redemption Window | Premature SGB redemption is only available on specific RBI-designated dates. Missing the window means waiting for the next eligible date or holding until final maturity. |

Gold works as a portfolio diversifier, with the right allocation depending on your goals, time horizon and risk profile. Since new SGBs are no longer available at issue price, building or rebalancing a gold position now means choosing between secondary-market SGBs, gold ETFs and gold mutual funds on cost, liquidity and post-tax returns, using a structured gold ETF vs SGB comparison as part of the decision.

At Right Horizons, our team can help you work out the right gold allocation as part of a broader financial plan suited to your goals. If you already hold SGBs nearing a five-year or eight-year mark, reviewing your retirement planning timeline alongside the RBI redemption calendar can help you decide whether to redeem or continue holding. Get in touch with us to review your gold strategy.

Talk to us

Investor Grievance

Talk to us

Investor Grievance