Estate planning in India ensures your assets are protected and distributed according to your wishes after your lifetime. Working with an experienced estate planning lawyer can help you create legally sound documents and avoid common succession-related issues. Without proper planning, families often face prolonged legal disputes, court cases, and assets distributed by succession laws that may not reflect your intentions. This guide covers everything you need to know about securing your financial legacy.

Estate planning is the systematic process of organizing your financial affairs to ensure assets are managed and distributed per your wishes. In India, this becomes complex due to diverse personal laws, joint family structures, and varying state regulations.

An effective estate plan, ideally reviewed by an estate planning lawyer, includes a legally valid will, beneficiary nominations, trusts for complex assets, powers of attorney, and business succession instructions. Without these, your assets could remain in probate courts for years, creating emotional and financial burdens for your family. Families managing significant wealth across asset classes often benefit from dedicated family office services to ensure continuity across generations.

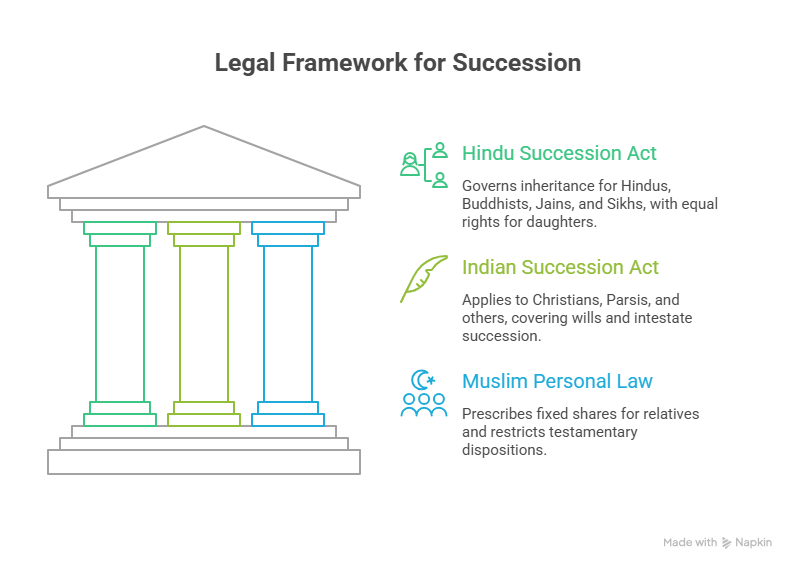

This act applies to Hindus, Buddhists, Jains, and Sikhs, governing both testamentary and intestate succession. The 2005 amendment gave equal inheritance rights to daughters in ancestral property. Under intestate succession, Class I heirs, including spouse, children, and mother, have the first claim, followed by Class II heirs such as father and siblings.

This governs Christians, Parsis, and others not covered by personal laws. It provides frameworks for will creation, probate procedures, and intestate succession. Probate is required for wills in former Presidency towns such as Mumbai, Kolkata, and Chennai, and can take months to years.

This personal law prescribes fixed statutory shares for relatives. Individuals governed by this law can create wills, but testamentary dispositions are restricted to one-third of the estate. The remaining two-thirds must be distributed according to the applicable personal law.

A will specifies how your assets should be distributed after death, who executes these instructions, and who cares for minor children. An estate planning lawyer can help ensure the will is drafted clearly and meets the legal requirements applicable to your situation.

For legal validity, the testator must be of sound mind and at least 18 years old. The will must be voluntary, signed by you on each page, and witnessed by two people who are not beneficiaries. Clear identification of the testator and a statement revoking previous wills are essential.

List all assets comprehensively including real estate, bank accounts, investments, jewelry, vehicles, and business interests. Name beneficiaries with full legal names and specify what each receives. Appoint a trustworthy executor and, if you have minor children, name a legal guardian.

While optional, registering your will at the Sub-Registrar’s office provides legal protection and creates a permanent record. Probate validates the will through courts and is mandatory in certain jurisdictions or recommended for complex estates.

Trusts offer flexibility beyond simple wills, particularly for complex estates or providing for family members with special needs.

A trust transfers assets to a trustee who manages them for beneficiaries. Unlike wills effective only after death, trusts can operate during your lifetime and continue afterward. Governed by the Indian Trusts Act, 1882, trusts require a written trust deed.

Family Trusts benefit family members across generations with conditions on inheritance timing. Testamentary Trusts are established through wills and activate after death. Charitable Trusts serve public benefit and offer tax advantages. Revocable Trusts allow modifications, while Irrevocable Trusts provide stronger asset protection.

Trusts enable continuous asset management, maintain privacy unlike wills which become public during probate, protect from creditors, and ensure ongoing support for dependents. They are particularly valuable for family businesses requiring professional management across generations. For families with complex, multi-generational wealth, private wealth management services can provide the ongoing oversight that trusts alone cannot.

A power of attorney, or POA, authorizes someone to act on your behalf if you become incapacitated. A General POA grants broad financial authority, Specific POA limits authority to particular transactions, and Durable POA remains effective during mental incapacity.

Healthcare directives express medical treatment preferences if you cannot communicate. While the legal framework is evolving in India, these documents guide families during critical decisions.

Though the Gift Tax Act was abolished in 1998, gifts are now taxable under Section 56(2) if exceeding ₹50,000 annually. Gifts from specified relatives such as spouse, siblings, parents, and lineal descendants are completely exempt, making strategic gifting an effective estate planning tool.

Assets transferred through inheritance pass the original cost and holding period to beneficiaries. However, lifetime sales or gifts may incur capital gains tax. Long-term capital gains on equity held over one year are taxed at 12.5% above ₹1.25 lakh. For a deeper look at managing these liabilities as your estate grows, read our guide on tax-efficient wealth management strategies for HNIs.

Estates generating income from rentals, deposits, or businesses must file tax returns until asset distribution. Once transferred, income becomes taxable in beneficiaries’ hands. Understanding tax planning for retirement in India can help ensure your estate plan and post-retirement income strategy are aligned.

Operating businesses through corporate structures like private limited companies or LLPs protects personal wealth from business liabilities. Shareholders’ agreements outline share transfer upon death, preventing division among disinterested heirs.

Life insurance provides immediate liquidity for expenses, debts, and taxes without forcing asset sales. Policies can equalize inheritances when one child receives a business while others receive insurance proceeds. Read our guide on securing your financial future through retirement planning to understand how insurance fits into a broader wealth preservation strategy.

Create detailed succession plans identifying successors, documenting processes, and establishing transition timelines. Buy-sell agreements funded by insurance ensure smooth ownership transfer between partners. Business owners can explore how Right Horizons supports entrepreneurs with financial and succession planning.

NRIs with assets across countries should create separate wills for each jurisdiction, simplifying probate and ensuring local law compliance. Understanding double taxation avoidance agreements, or DTAA, prevents tax duplication. If you are an NRI managing investments in India, our financial planning guide for NRIs covers the key strategies you need to consider. Right Horizons’ dedicated NRI services are designed to address the unique cross-border financial planning needs of the Indian diaspora.

Special needs trusts provide financial support while maintaining government benefit eligibility. Trustees must understand the beneficiary’s needs and benefit rules for long-term fund management.

Document all digital assets including email accounts, social media profiles, cryptocurrency wallets, online payment platforms, and cloud storage. Store access instructions securely using password managers your executor can access. Specify in your will what happens to each digital asset type.

Procrastination is the biggest mistake. Start with basic documents regardless of age or wealth. Failing to update your plan after marriages, divorces, births, or deaths creates misalignment with current wishes. Ignoring nominations that do not match your will creates confusion. Lack of liquidity planning may force asset sales at unfavorable prices. Diversifying across asset classes before and during estate planning can reduce this risk — our guide on alternative investment options explains how broader diversification supports long-term wealth preservation.

Inventory Assets: List real estate, accounts, investments, retirement funds, business interests, vehicles, jewelry, and digital assets. Understanding best asset allocation methods can help you assess the structure of your current portfolio before drafting your plan.

Define Goals: Determine who receives which assets, conditions on inheritances, provisions for dependents, charitable intentions, and business succession plans.

Choose Key People: Select executors, trustees, guardians for minors, and power of attorney agents.

Draft Documents: Work with an estate planning lawyer and other professionals to create wills, trust deeds, and powers of attorney that comply with legal requirements.

Execute Properly: Sign documents with proper witnessing. Consider registering your will for added protection.

Communicate: Inform key family members about document locations and your general intentions.

Review Regularly: Update every three years or after major life events.

Estate planning requires legal, financial, and tax expertise. An estate planning lawyer ensures legal compliance, prepares comprehensive documentation, and helps reduce the risk of disputes among beneficiaries. Financial planners integrate estate planning into your overall financial picture, while an estate planning lawyer focuses on the legal structure of your will, trust, nominations, and succession documents. Tax consultants minimize liabilities for your estate and beneficiaries. Insurance advisors structure policies for your specific goals.

Estate planning protects your family’s financial security and provides peace of mind. Whether you need a simple will or comprehensive planning involving trusts and business succession, guidance from an estate planning lawyer ensures your plan is legally sound and reflects your wishes.

Schedule a consultation with our financial planning team today to discuss your estate planning needs.

Talk to us

Investor Grievance

Talk to us

Investor Grievance