| Key Takeaways |

|---|

| • Diversification performance metrics are essential tools for measuring portfolio efficiency and risk-adjusted returns |

| • Core metrics include Sharpe ratio, Treynor ratio, and Information ratio for risk-adjusted returns, and standard deviation, beta, and correlation coefficients for portfolio risk |

| • Advanced metrics like diversification ratio, portfolio entropy, and effective number of bets provide deeper insights into portfolio diversification |

| • Practical application of these metrics involves portfolio construction, performance attribution, and risk management |

| • Future trends in diversification performance measurement include AI applications and integration with ESG investing |

Diversification performance metrics are vital for evaluating and optimizing investment portfolios. These tools help investors and financial professionals assess the effectiveness of their diversification strategies, leading to improved risk-adjusted returns. By using these metrics, investors can make informed decisions about asset allocation, risk management, and portfolio rebalancing.

Diversification performance metrics are quantitative measures used to evaluate the effectiveness of portfolio diversification strategies. These metrics are essential for investors and portfolio managers seeking to optimize their investment strategies and achieve superior risk-adjusted returns. The primary objectives of measuring diversification performance include:

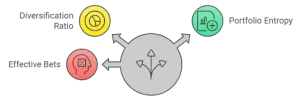

The diversification ratio quantifies the level of diversification within a portfolio by comparing the weighted average of individual asset volatilities to the overall portfolio volatility. A higher ratio indicates better diversification.

Portfolio entropy, derived from information theory, measures the dispersion of weights across different assets or strategies within a portfolio. Higher entropy suggests more balanced diversification.

This metric estimates the number of independent risk factors or “bets” within a portfolio, providing insights into the true level of diversification beyond simple asset count.

For equity portfolios, specific metrics such as sector concentration, factor exposure, and geographic diversification are crucial. These metrics help investors assess the balance and potential risks within their equity allocations.

Fixed income diversification can be evaluated using metrics like duration, credit quality distribution, and yield curve positioning. These measures provide insights into the portfolio’s sensitivity to interest rate changes and credit risk.

Alternative investments require unique diversification metrics, such as strategy correlation, drawdown analysis, and liquidity profiles. These metrics help investors understand the role of alternatives in their overall portfolio diversification.

Diversification metrics play a crucial role in the portfolio construction process. By analyzing these metrics, investors can identify opportunities to enhance diversification and optimize their asset allocation strategies.

Performance attribution analysis uses diversification metrics to understand the sources of portfolio returns and risk. This helps investors and managers identify which aspects of their diversification strategy are contributing positively or negatively to overall performance.

Ongoing monitoring of diversification metrics is essential for effective risk management. Regular assessment of these metrics allows investors to identify potential concentration risks and make necessary adjustments to maintain desired diversification levels.

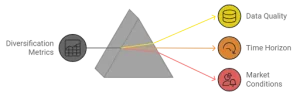

Accurate diversification metrics rely on high-quality, comprehensive data. Limited or poor-quality data can lead to misleading results and suboptimal decision-making.

Diversification benefits and metrics can vary significantly across different time horizons. Short-term correlations may not reflect long-term diversification effects, requiring careful interpretation of metrics over various periods.

During extreme market events, traditional diversification relationships may break down, leading to unexpected portfolio behavior. Investors must be aware of these limitations when relying on historical diversification metrics.

Advanced machine learning algorithms and artificial intelligence are increasingly being applied to diversification analysis, enabling more sophisticated pattern recognition and predictive modeling of diversification effects.

The advent of big data and advanced analytics is facilitating real-time monitoring of diversification metrics, allowing for more dynamic and responsive portfolio management.

As ESG investing and factor-based strategies gain prominence, diversification metrics are evolving to incorporate these dimensions, providing a more holistic view of portfolio diversification.

Diversification performance metrics are indispensable tools for modern portfolio management, offering valuable insights into risk-adjusted returns and portfolio efficiency. By employing a comprehensive set of metrics, investors can make more informed decisions about asset allocation, risk management, and portfolio optimization. However, it is crucial to recognize that quantitative metrics should be balanced with qualitative analysis and a deep understanding of market dynamics.

As the investment landscape continues to evolve, so too will the sophistication and application of diversification performance metrics, ultimately leading to more robust and efficient portfolio management strategies. For investors looking to enhance their portfolio diversification and performance, consulting with a financial advisor can provide valuable guidance in applying these metrics effectively.

Retirement planning and tax planning are also important considerations when implementing diversification strategies, as they can significantly impact long-term investment outcomes.

Talk to us

Investor Grievance

Talk to us

Investor Grievance